Software & Private Credit

“When sorrows come, they come not single spies / but in battalions"

For the better part of the past fifteen years, since after the global financial crisis, the technology sector in the US has been in a secular growth trend. Specifically, software and software-adjacent sectors are considered to be asset-light investments with high recurring revenues, and for this reason preferred by public and private investors alike.

The story is beginning to change, as the growing capabilities of AI are leading investors to rethink the software industry’s fundamentals. The recent product rollouts by Anthropic’s Claude and OpenAI are disrupting the traditional SaaS model by allowing users with little to no coding experience to build software, driving enterprise software costs down significantly. The software companies poised to benefit from the advancements in AI, are now at risk of being wiped out because of it.

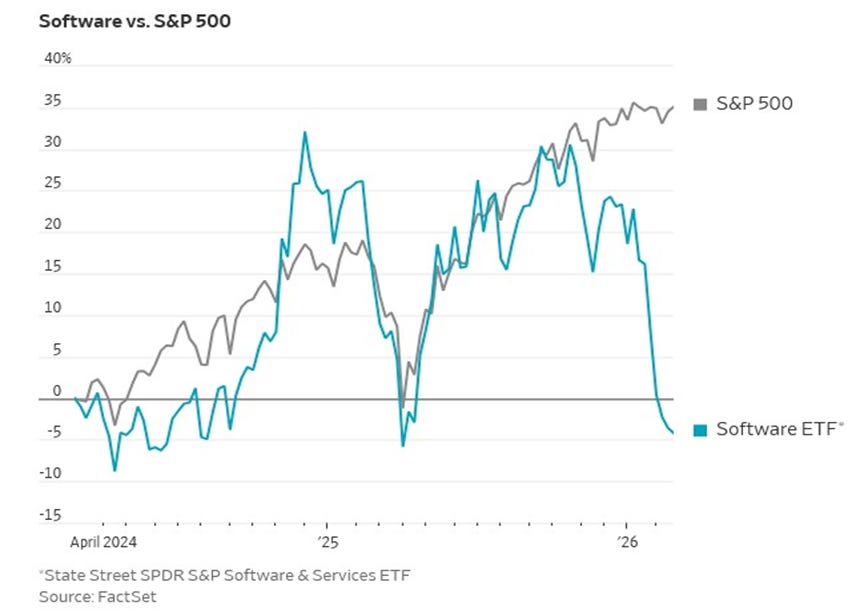

Safe to say, the technology industry as an asset class has had an eventful few months, and investors are fleeing the software sector en masse:

Another sector that’s had great success since the crisis is private credit. The sector has seen huge inflows in the wake of increased regulation on the banking sector and has benefited from a consistently low rate environment. Institutional investors (pensions, endowments, insurers) starved for yield poured into private credit, which the industry capitalized on with high leverage.

The story here too, is beginning to change. The asset class is now facing the test with rising defaults, troubled loans, and narrowing loan margins, among other things, that are fueling negative sentiment, and a rush to the exits for investors. From the FT:

Back to the software sector for a moment. If you, whether as a VC in the private space, or an equity investor in capital markets, have been involved in the software sector any time in the past 15 years, you were aware of the game you (and the market) were playing. The formula goes; you invest in a basket of promising technology companies, and even if a couple of them have lackluster returns, you hope to come out ahead if a few of them do exceptionally well.

So today if you’re one of those participants, you’re thinking ‘well, we had a good run. Now we need to assess if AI will really enhance or replace the software industry or this particular software stock as it exists. If it’s the former, we double down on it. If it’s the latter, we move on to better pastures’. Pretty routine.

Lenders, on the other hand, do not have the same privilege. Creditors do their due diligence not really on the multiple expansion, but on predictable, recurring cash flows to cover interest payments and hope to get repaid at maturity. But what happens when the cashflows that seemed predictable and recurring don’t seem so anymore?

Again from the FT:

“Investors are souring on listed private credit funds that lend to software companies as concerns grow over AI’s potential to disrupt their business models and eat into their profits.”

“Bonds and shares of business development companies (BDCs), which make loans to middle-market groups, have also fallen sharply, despite a rebound on Friday and Monday, highlighting the large exposure that the private credit industry has built to the sector in recent years.”

Direct Lending to software companies, more specifically to SaaS, gained and ballooned in recent years for the profit margins, stable customer bases, and reliable subscription revenues. Most of these software loans came at the height of software valuations in the ultra-low interest rates after 2020. The underwriting based on growth assumptions made in better times is being stress-tested by the AI industry in much less forgiving times for the industry.

Then there’s the categorization issue. Bloomberg reports that in the BDC space ‘at least 250 loans to software firms worth more than $9 billion’ are miscategorized as non-software industries. There are several firms in the insurance, real estate, and logistics space that are in reality software providers for those industries, and directly exposed to AI risk.

Software dominates BDC loanbooks. 20% of BDC loans are exposed to software firms, with more than one-third of their loans linked to software having suffered widening spread. The issue for investors in software-heavy BDCs, unlike those in publicly traded software firms as we talked above (you can just take your money out), is what happens from now till maturity. The situation here at face value reflects something like the inverse of an illiquidity premium, hence the recoil reaction from the market.

In the face of growing AI use-cases, software-heavy public BDCs from here on could be impacted from both ends; wider spreads and credit downgrades risk raising their borrowing costs, and on the other side, increasing restlessness and panic feeding into redemptions (and all that comes with it).